Anton Shestakov

May 12, 2025

The debt collection model banks have relied on for decades is breaking down. Call centers, manual phone calls, and unstructured follow-ups are proving too costly, too inflexible, and too damaging to the customer experience. As loan portfolios grow and customer expectations evolve, traditional approaches are falling short—leading to stagnating recovery rates and rising operational costs.

The automation conversation is shifting. Most banks today already use some form of automation—but the real question is no longer whether to automate, but how effectively you’re doing it. The old debate of “humans vs. AI” is outdated. What matters now is whether your automation is smart enough to deliver results. And that’s where many institutions are stuck—still relying on first-generation bots that are cheap, scalable, and easy to deploy, but ultimately limited. These bots lack persistence, adaptability, and intelligence. Customers recognize them instantly—and often, ignore them just as quickly.

Conversational AI changes the game. It blends the emotional intelligence of human agents with the scalability of automation, delivering real-time, personalized communication across multiple channels. It adapts. It learns. And it performs—helping banks like TBC Uzbekistan increase collection efficiency by 10x per $1,000 collected, while reducing overhead and improving customer satisfaction.

The future of debt collection isn’t human vs. bot. It’s about finding the intelligent middle ground. And that’s exactly where Aiphoria leads.

Challenges of traditional debt collection and legacy automation

Historically, debt collection has relied heavily on human agents to personally engage with customers and recover overdue payments. While human collectors can be persistent and persuasive, they present significant operational challenges. They are expensive to recruit, train, and retain, and they require ongoing investment in compliance, supervision, and HR infrastructure. More critically, scaling human teams is both slow and inefficient—especially when delinquency volumes fluctuate. When banks need to ramp up quickly, they face recruitment bottlenecks; when volumes drop, scaling down incurs high attrition costs such as severance, exit bonuses, and knowledge loss.

This lack of agility becomes particularly problematic during seasonal and macroeconomic shifts. For instance, delinquency often dips at the end of December and spikes again in January or February. Banks are left overstaffed during slow periods, yet under-resourced during peak recovery windows. Even within a single month, workloads can spike temporarily—such as around payday—when the window for follow-up may shrink to just a few days. Traditional teams simply can’t adjust fast enough to match these short bursts of intensity.

Attempting to address these scalability and cost issues, financial institutions adopted the first generation of automation—basic, rule-based bots. These bots were affordable and easy to scale, but their interactions were impersonal, predictable, and ineffective. Customers quickly recognized when they were interacting with a bot and learned how to dismiss or bypass the automated conversations, often ending calls without genuine payment commitments. Moreover, these legacy systems lacked the capacity to learn or adapt, rendering them incapable of handling the sensitive nuances inherent in debt recovery conversations.

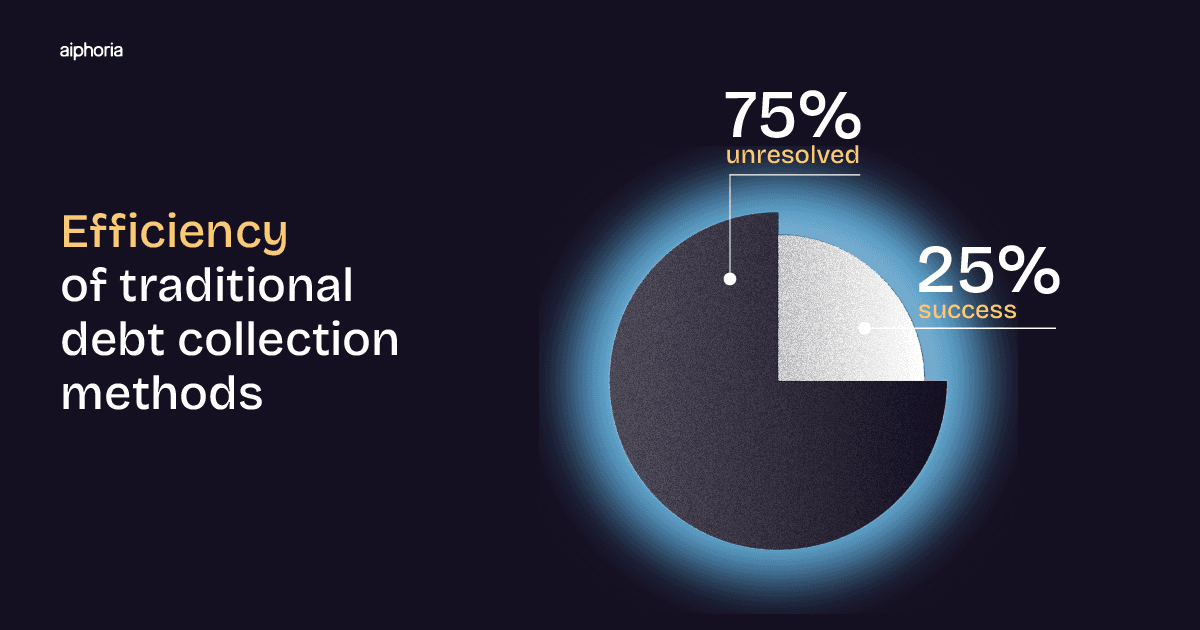

McKinsey & Company reports illustrate this ineffectiveness clearly: traditional phone calls achieve only about a 12% full-payment success rate, highlighting that conventional outreach channels struggle significantly to secure complete debt resolution. Conversely, advanced digital channels, particularly those providing personalized, interactive, and responsive communication, consistently achieve substantially higher engagement and payment outcomes.

Today, financial institutions require solutions that blend scalability with humanlike, nuanced interactions. Unlike outdated automation, conversational AI debt collection leverages adaptive, sentiment-aware dialogues that respect individual customer circumstances. Conversational AI solutions integrate self-learning capabilities, ensuring personalized and respectful engagement that substantially improves both debt recovery rates and customer satisfaction—addressing precisely the gaps left by legacy systems.

Surveys by McKinsey & Company and PwC

How Conversational AI addresses these issues

Conversational AI represents the ideal balance between the strengths and weaknesses of human agents and first-generation bots in debt collection. It combines the persistence and nuanced engagement offered by human collectors with the affordability and scalability of automation. By intelligently adapting conversations in real-time, conversational AI ensures respectful, personalized interactions—significantly improving recovery rates, reducing operational costs, and enhancing customer experiences.

As financial institutions continue to evolve their debt collection strategies, there is a growing need for a solution that strikes a balance between automation and human interaction. This is where conversational AI comes in, offering a bridge between traditional, basic bots and expensive human agents. It provides a unique combination of the reach and scalability of automation, while maintaining the emotional intelligence necessary to manage sensitive situations with customers.

Our research highlights 6 key benefits of adopting conversational AI debt collection processes across every stage of the debt recovery journey. Conversation AI is:

Cheaper than Human Collectors

One of the primary benefits of conversational AI is that it is cheaper than human collectors. According to a study by The Kaplan Group, AI automation can result in operational cost reductions of between 30% and 50%. While human agents are still essential in certain complex cases, their involvement comes at a significant cost—not just in terms of salaries but also the risk of burnout and operational inefficiency. Conversational AI provides a scalable solution that reduces reliance on human collectors, allowing institutions to handle a much larger volume of interactions at a fraction of the cost. It offers an effective way to automate without sacrificing the quality of service, making it a highly cost-efficient option.

More Effective and Nuanced than Old-School Bots

Furthermore, conversational AI is more effective and nuanced than old-school bots. Early automation systems were designed to handle basic tasks. However, they often fell short when it came to dealing with more complex, emotionally charged interactions. Customers soon became aware of their limitations, which led to disengagement and ineffective resolutions. In contrast, conversational AI employs advanced machine learning and natural language processing, allowing it to engage in real-time, human-like conversations that are sensitive to the customer's tone, intent, and emotional state. This level of sophistication leads to much better customer engagement, ultimately resulting in higher chances of successful debt recovery.

Self-Training Over Time = Long-Term Efficiency Gains

A key advantage of conversational AI is its ability to self-train over time, making it increasingly efficient. Unlike traditional bots, which rely on rigid rule-based programming, conversational AI continuously learns from every interaction. With each conversation, it improves its responses and predictions, becoming more accurate and effective as time goes on. This self-improvement leads to long-term efficiency gains, ensuring that the system continues to adapt to changing customer behavior and economic conditions, delivering optimal results without needing constant manual intervention.

Adaptable Enough to Engage Customers Without Harming Satisfaction Scores

Additionally, conversational AI is designed to be adaptable. Debt collection often involves sensitive situations where customers may already be under financial stress. Traditional bots lacked the emotional intelligence required to navigate these delicate conversations, often resulting in frustration and negative experiences. Conversational AI, however, is specifically built to detect and respond to emotional cues in customer interactions. This allows it to engage with customers in a consistent and controlled manner, adapting to different scenarios while ensuring that the collection process remains respectful, compliant, and effective—without the risk of emotional escalation. By providing context-aware responses, conversational AI fosters better relationships with customers, boosting satisfaction and ultimately increasing the chances of successful debt resolution.

Scalable in line with Bank Operations

Conversational AI solutions scale effortlessly in line with a bank’s evolving portfolio. Unlike human teams—which face hiring, training, and capacity challenges—AI agents can be deployed instantly and in any volume. As delinquency increases, banks can simply activate more AI agents without additional cost, onboarding, or quality loss. This ensures that the collection rate and cost per $1,000 recovered remain stable, even during periods of rapid portfolio growth.

Beyond growth, conversational AI is also critical for managing fluctuations—whether seasonal or macroeconomic. For example, delinquency often drops in December but spikes in January and February. Human teams can’t easily scale down and back up without incurring significant costs and inefficiencies. With AI, there's no downtime cost and no lag—capacity can be scaled up or down instantly, with consistent performance.

Even within a single month, workloads can shift sharply—such as around payday when outreach intensity needs to peak for just a few days. Conversational AI allows banks to precisely match effort to demand, maximizing efficiency exactly when it matters most. Combined with real-time follow-ups and intelligent outreach, this dynamic scalability accelerates recovery and improves overall financial performance.

Easily Adaptable to regulatory evolution

Conversational AI systems can be configured to strictly comply with evolving financial regulations, ensuring every customer interaction meets legal and industry standards. This adaptability helps reduce regulatory risk while maintaining trust and consistency across all outreach channels.

Source: The Kaplan Group & Aiphoria

Expert Insight: Aiphoria CPO Natalya Savinova on the Future of AI Debt Collection

At Aiphoria, we specialize in AI-powered virtual employees that help customer support channels automate high friction processes. One of our main areas of expertise is helping financial institutions transition from manual to AI-powered collection strategies. Based on this experience, our Chief Product Officer, Natalya Savinova, shared valuable insights on what banks should expect—and how to implement AI debt collection effectively.

The Hidden Cost of Manual Collection

Natalya explained, “Humans have traditionally been highly effective at debt collection because they can communicate with persistence and persuasion. However, relying exclusively on human agents is extremely expensive for companies and puts significant psychological pressure on collectors. Over time, this pressure can lead to burnout, impatience, and ultimately, poor customer experiences that damage satisfaction and loyalty. Attrition becomes a real issue as well: as banks grow, scaling human teams up means increased labor costs, and scaling them down is equally challenging due to severance payments and exit costs. Consequently, staffing rarely aligns perfectly with a fluctuating portfolio size.”

Natalya emphasized that conversational AI solves these challenges by striking the perfect balance between the intelligence and effectiveness of human agency and the cost efficiency of automation.

“Conversational AI sits precisely in that ideal middle ground,” she said.

It’s cheaper and more scalable than human collectors, but dramatically more effective—than basic bots.

It engages customers intelligently

It can learn and adapt in real time, while maintaining respectful conversations.

Banks using conversational AI thus achieve efficient debt recovery, lower costs, and higher customer satisfaction. This combination positions conversational AI as the clear win-win-win solution, making it a no-brainer choice for banking looking for operational efficiency compared to first-generation bots.

Four Steps Every Bank Should Take to Implement AI Debt Collection Effectively

Natalya then outlined five essential steps for banks to effectively implement conversational AI:

Define the Process – “Clearly map out your collection workflows, communication strategies, rules and restrictions, and success criteria to ensure precise requirements for AI and predictable result.”

Supply AI with Real Data – “Utilize actual employee instructions, historical call logs and payment data to develop intelligent, context-aware AI tailored to your processes and real customer behaviors.”

Integrate Key Systems – “Connect your AI tools seamlessly with existing CRMs, communication platforms, and core banking systems, ensuring real-time data access and effective responses.”

Measure and Iterate - “Track KPIs and evaluate conversation quality to improve for advanced results. Manage change gradually – if you are not comfortable with fully autonomous AI yet, then introduce it as a supportive co-pilot alongside human agents to build trust, enable smooth adoption, and continuously refine.”

Natalya stated firmly, “Without these foundational steps, even the most sophisticated conversational AI solution will not realize its full potential.”

Conclusion

The future of debt collection lies not in replacing humans outright, nor in relying on outdated, rule-based bots—but in embracing conversational AI as the intelligent middle ground. As banks scale, they face increasing pressure to balance cost, compliance, and customer experience. Traditional approaches—whether high-touch human teams or rigid legacy automation—simply can’t adapt fast enough.

Conversational AI, as demonstrated by institutions like TBC Uzbekistan, delivers the scalability of automation, the persistence of human interaction, and the intelligence to continuously learn and improve. It empowers banks to engage customers through real-time, personalized conversations across multiple channels—driving better recovery rates while preserving long-term relationships.

Unlike first-generation bots that are static, easily bypassed, and incapable of nuanced engagement, Aiphoria’s platform creates dynamic, respectful, and efficient interactions that adjust to customer behavior. The result is not only better performance, but a true competitive edge in today’s increasingly customer-centric financial landscape.

👉 DM Aiphoria to Book a demo to see how Aiphoria’s conversational AI can transform your collections process.

Sources:

Anton Shestakov